Python

Build & Use Sector Rotation Charts for Smarter Investing with Python

FabTrader

Article overview

Learn how to build and interpret sector rotation charts in Python to compare relative strength, spot leadership shifts, and make more informed investing decisions.

In the world of investing and trading, identifying market leaders and laggards is crucial. Traditional price charts and indicators provide valuable insights, but they often fail to visualize sector or stock rotation in a clear and intuitive manner. This is where sector rotation charts come into play.

Sector rotation charts allow traders and investors to compare the relative strength and momentum of multiple securities against a benchmark, revealing how different stocks, sectors, or asset classes are rotating through various performance phases. This article explores how to interpret these charts effectively and use them for making informed investment decisions.

What Is a Sector Rotation Chart?

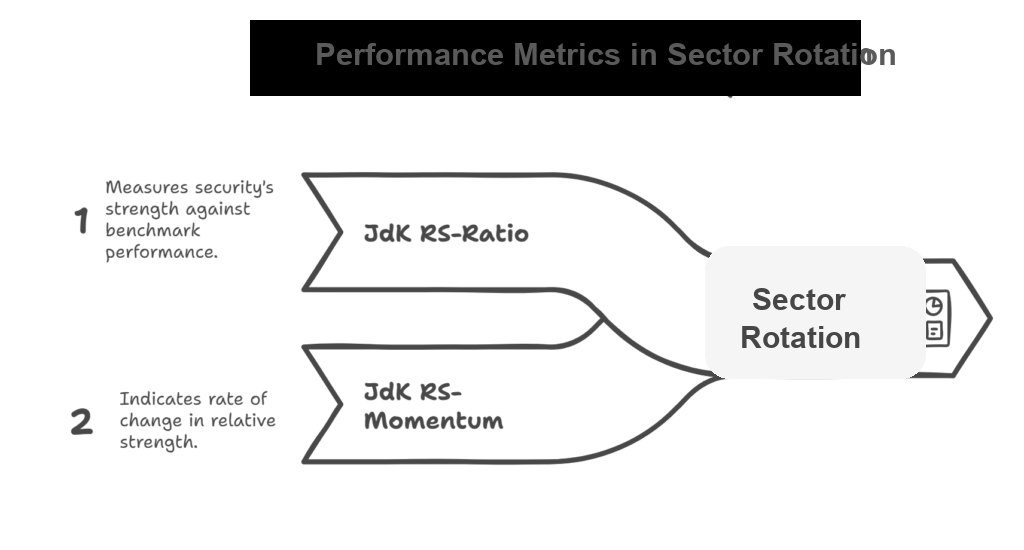

A sector rotation chart is a visualization tool that plots securities based on two key indicators:

- JdK RS-Ratio (Relative Strength Ratio) – Measures a security’s relative strength against a benchmark. Higher values indicate outperformance, while lower values suggest underperformance.

- JdK RS-Momentum (Relative Strength Momentum) – Measures the rate of change of the relative strength. Increasing momentum suggests improving strength, while decreasing momentum signals weakening performance.

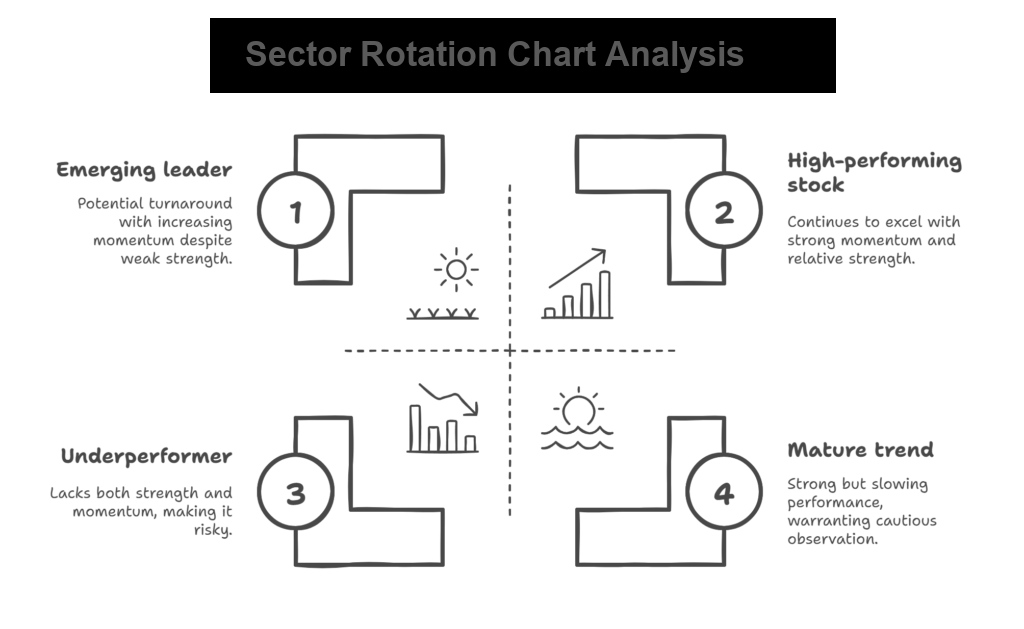

By plotting these values on a two-dimensional plane, the chart naturally divides into four quadrants:

Improving (Look for Buys) – Top-left quadrant

- Securities in this quadrant have weak relative strength but are gaining momentum.

- These are potential turnaround candidates that may soon transition into the leading quadrant.

- Ideal for investors looking for early entry points into emerging leaders.

Leading (Hold) – Top-right quadrant

- Securities in this quadrant have both high relative strength and strong momentum.

- These are the outperformers of the market.

- Typically, stocks or sectors here continue to perform well, making them attractive for holding or further accumulation.

Weakening (Look for Sells) – Bottom-right quadrant

- Securities in this quadrant still have high relative strength but are losing momentum.

- This often indicates a mature uptrend that may be slowing down.

- If a security remains in this quadrant for an extended period, it may transition into the lagging quadrant, signaling a potential exit point.

Lagging (Avoid) – Bottom-left quadrant

- Securities in this quadrant exhibit both weak relative strength and weak momentum.

- These are underperformers that should be avoided or shorted.

- Investors should be cautious about bottom fishing unless there is a clear sign of reversal.

Access this Tool for free on our community site

You can access this tool here

Python Implementation

Following is the Python Streamlit implementation of the sector rotation chart.

import streamlit as st

import yfinance as yf

import pandas as pd

import numpy as np

import plotly.graph_objects as go

import plotly.express as px

from datetime import datetime, timedelta

import warnings

from scipy.interpolate import interp1d

warnings.filterwarnings('ignore')

# Configure page

st.set_page_config(

page_title="Sector Rotation Analysis",

layout="centered"

)

# Apply fixed screen width for app (1440px)

st.markdown(

f"""

<style>

.stAppViewContainer .stMain .stMainBlockContainer{{ max-width: 1440px; }}

</style>

""",

unsafe_allow_html=True,

)

def fetch_data(symbols, period_days):

"""Fetch data from Yahoo Finance with error handling"""

data = {}

failed_symbols = []

# Calculate start date

end_date = datetime.now()

start_date = end_date - timedelta(days=period_days + 10) # Add buffer for calculations

for symbol in symbols:

try:

hist = yf.download(symbol, start_date, end_date, multi_level_index=False)

if len(hist) < 20: # Minimum data requirement

failed_symbols.append(symbol)

continue

data[symbol] = hist['Close']

except Exception as e:

failed_symbols.append(symbol)

continue

return data, failed_symbols

def calculate_relative_strength(price_data, benchmark_data, period):

"""Calculate relative strength vs benchmark"""

# Ensure we have enough data

min_length = min(len(price_data), len(benchmark_data))

if min_length < period:

return None, None

# Align data by index

aligned_data = pd.DataFrame({

'price': price_data,

'benchmark': benchmark_data

}).dropna()

if len(aligned_data) < period:

return None, None

# Calculate relative strength (sector/benchmark)

relative_strength = aligned_data['price'] / aligned_data['benchmark']

# Calculate momentum (rate of change)

rs_momentum = relative_strength.pct_change(period).dropna()

return relative_strength, rs_momentum

def calculate_jdk_rs_ratio(relative_strength, short_period=10, long_period=40):

"""Calculate JdK RS-Ratio similar to sector rotation methodology"""

if len(relative_strength) < long_period:

return None

# Normalize relative strength to 100

rs_normalized = (relative_strength / relative_strength.rolling(long_period).mean()) * 100

return rs_normalized

def calculate_jdk_rs_momentum(rs_ratio, period=10):

"""Calculate JdK RS-Momentum"""

if rs_ratio is None or len(rs_ratio) < period:

return None

# Calculate momentum as rate of change

momentum = ((rs_ratio / rs_ratio.shift(period)) - 1) * 100

return momentum

def get_quadrant_info(rs_ratio, rs_momentum):

"""Determine quadrant and provide info"""

if rs_ratio > 100 and rs_momentum > 0:

return "Leading", "green", "🚀"

elif rs_ratio > 100 and rs_momentum < 0:

return "Weakening", "orange", "📉"

elif rs_ratio < 100 and rs_momentum < 0:

return "Lagging", "red", "📊"

else:

return "Improving", "blue", "📈"

def smooth_data(x_vals, y_vals, method="Moving Average", window=3):

"""Smooth the tail data using various methods"""

if len(x_vals) < 3 or len(y_vals) < 3:

return x_vals, y_vals

try:

if method == "Moving Average":

# Simple moving average

x_smooth = pd.Series(x_vals).rolling(window=window, center=True, min_periods=1).mean().values

y_smooth = pd.Series(y_vals).rolling(window=window, center=True, min_periods=1).mean().values

elif method == "Exponential":

# Exponential smoothing

alpha = 2.0 / (window + 1)

x_smooth = pd.Series(x_vals).ewm(alpha=alpha, adjust=False).mean().values

y_smooth = pd.Series(y_vals).ewm(alpha=alpha, adjust=False).mean().values

elif method == "Spline":

# Spline interpolation for smoothing

if len(x_vals) >= 4: # Need at least 4 points for cubic spline

indices = np.arange(len(x_vals))

# Create more points for smoother curve

new_indices = np.linspace(0, len(x_vals) - 1, len(x_vals) * 2)

# Interpolate

f_x = interp1d(indices, x_vals, kind='cubic', bounds_error=False, fill_value='extrapolate')

f_y = interp1d(indices, y_vals, kind='cubic', bounds_error=False, fill_value='extrapolate')

x_smooth = f_x(new_indices)

y_smooth = f_y(new_indices)

# Sample back to original length but smoothed

sample_indices = np.linspace(0, len(x_smooth) - 1, len(x_vals)).astype(int)

x_smooth = x_smooth[sample_indices]

y_smooth = y_smooth[sample_indices]

else:

# Fall back to moving average for short series

x_smooth = pd.Series(x_vals).rolling(window=2, center=True, min_periods=1).mean().values

y_smooth = pd.Series(y_vals).rolling(window=2, center=True, min_periods=1).mean().values

return x_smooth, y_smooth

except Exception as e:

# If smoothing fails, return original data

return x_vals, y_vals

def create_sector_rotation_plot(results, tail_length, enable_smoothing=True, smoothing_method="Moving Average",

smoothing_window=3, show_tail=False):

"""Create the sector rotation chart"""

fig = go.Figure()

# First, determine the actual data ranges

all_rs_ratios = []

all_rs_momentum = []

for symbol, data in results.items():

if data['rs_ratio'] is not None and data['rs_momentum'] is not None:

rs_ratio_vals = data['rs_ratio'].dropna().values

rs_momentum_vals = data['rs_momentum'].dropna().values

if len(rs_ratio_vals) > 0 and len(rs_momentum_vals) > 0:

all_rs_ratios.extend(rs_ratio_vals)

all_rs_momentum.extend(rs_momentum_vals)

if not all_rs_ratios or not all_rs_momentum:

st.error("No valid data to plot")

return None

# Calculate dynamic ranges with some padding

x_min, x_max = min(all_rs_ratios), max(all_rs_ratios)

y_min, y_max = min(all_rs_momentum), max(all_rs_momentum)

# Add padding (10% on each side)

x_padding = (x_max - x_min) * 0.1

y_padding = (y_max - y_min) * 0.1

x_range = [x_min - x_padding, x_max + x_padding]

y_range = [y_min - y_padding, y_max + y_padding]

# Ensure 100 is visible on x-axis and 0 is visible on y-axis

x_center = 100

x_data_range = max(x_max - 100, 100 - x_min) # Get the larger distance from 100

x_range = [x_center - x_data_range - x_padding, x_center + x_data_range + x_padding]

if y_range[0] > 0:

y_range[0] = min(y_range[0], -0.5)

if y_range[1] < 0:

y_range[1] = max(y_range[1], 0.5)

# Add quadrant backgrounds based on actual ranges

fig.add_shape(

type="rect",

x0=100, y0=0, x1=x_range[1], y1=y_range[1],

fillcolor="rgba(0,255,0,0.1)",

line=dict(color="rgba(0,0,0,0)"),

name="Leading"

)

fig.add_shape(

type="rect",

x0=100, y0=y_range[0], x1=x_range[1], y1=0,

fillcolor="rgba(255,165,0,0.1)",

line=dict(color="rgba(0,0,0,0)"),

name="Weakening"

)

fig.add_shape(

type="rect",

x0=x_range[0], y0=y_range[0], x1=100, y1=0,

fillcolor="rgba(255,0,0,0.1)",

line=dict(color="rgba(0,0,0,0)"),

name="Lagging"

)

fig.add_shape(

type="rect",

x0=x_range[0], y0=0, x1=100, y1=y_range[1],

fillcolor="rgba(0,0,255,0.1)",

line=dict(color="rgba(0,0,0,0)"),

name="Improving"

)

# Add center lines

fig.add_hline(y=0, line_dash="dash", line_color="black", opacity=0.5)

fig.add_vline(x=100, line_dash="dash", line_color="black", opacity=0.5)

colors = px.colors.qualitative.Set2

for i, (symbol, data) in enumerate(results.items()):

if data['rs_ratio'] is None or data['rs_momentum'] is None:

continue

rs_ratio = data['rs_ratio'].dropna()

rs_momentum = data['rs_momentum'].dropna()

# Get the last 'tail_length' points

tail_points = min(tail_length, len(rs_ratio))

if tail_points < 2:

continue

x_vals = rs_ratio.tail(tail_points).values

y_vals = rs_momentum.tail(tail_points).values

# Apply smoothing if enabled

if enable_smoothing and tail_points > 2:

x_vals_smooth, y_vals_smooth = smooth_data(x_vals, y_vals, smoothing_method, smoothing_window)

else:

x_vals_smooth, y_vals_smooth = x_vals, y_vals

color = colors[i % len(colors)]

# Add tail (trajectory) - use smoothed data for the line, original for markers

if show_tail:

fig.add_trace(go.Scatter(

x=x_vals_smooth,

y=y_vals_smooth,

mode='lines',

name=f'{symbol} Trail',

line=dict(color=color, width=3, shape='spline' if smoothing_method == "Spline" else 'linear'),

opacity=0.7,

showlegend=False

))

# Add small markers along the trail (using original data)

if not enable_smoothing or len(x_vals) <= 5:

# Show more markers when not smoothing or short tail

marker_step = max(1, len(x_vals) // 8)

else:

# Fewer markers when smoothing for cleaner look

marker_step = max(2, len(x_vals) // 5)

# Add current position (larger marker) - always use original data

current_quad, quad_color, quad_icon = get_quadrant_info(x_vals[-1], y_vals[-1])

fig.add_trace(go.Scatter(

x=[x_vals[-1]],

y=[y_vals[-1]],

mode='markers+text',

name=f'{symbol} ({current_quad})',

marker=dict(

size=20,

color=color,

line=dict(width=2, color='white')

),

text=[f'{symbol}'],

textposition="middle right",

textfont=dict(size=15, color='black'),

hovertemplate=f'<b>{symbol}</b><br>' +

f'RS-Ratio: {x_vals[-1]:.2f}<br>' +

f'RS-Momentum: {y_vals[-1]:.2f}<br>' +

f'Quadrant: {current_quad}<extra></extra>'

))

# Update layout

fig.update_layout(

xaxis_title="RS-Ratio",

yaxis_title="RS-Momentum",

width=800,

height=1000,

showlegend=False,

legend=dict(

orientation="v",

yanchor="top",

y=1,

xanchor="left",

x=1.01

)

)

# Set dynamic axis ranges

fig.update_xaxes(range=x_range)

fig.update_yaxes(range=y_range)

# Add annotations for quadrants - position them based on actual ranges

x_mid = (x_range[0] + x_range[1]) / 2

y_mid = (y_range[0] + y_range[1]) / 2

# Leading quadrant (top-right)

leading_x = (100 + x_range[1]) / 2

leading_y = y_range[1] * 0.8

fig.add_annotation(x=leading_x, y=leading_y, text="Leading<br>(Hold Position)",

# showarrow=False, font=dict(size=14, color="green"))

showarrow=False, font=dict(size=14))

# Weakening quadrant (bottom-right)

weakening_x = (100 + x_range[1]) / 2

weakening_y = y_range[0] * 0.8

fig.add_annotation(x=weakening_x, y=weakening_y, text="Weakening<br>(Look to Sell)",

# showarrow=False, font=dict(size=14, color="orange"))

showarrow=False, font=dict(size=14))

# Lagging quadrant (bottom-left)

lagging_x = (x_range[0] + 100) / 2

lagging_y = y_range[0] * 0.8

fig.add_annotation(x=lagging_x, y=lagging_y, text="Lagging<br>(Avoid)",

# showarrow=False, font=dict(size=14, color="red"))

showarrow=False, font=dict(size=14))

# Improving quadrant (top-left)

improving_x = (x_range[0] + 100) / 2

improving_y = y_range[1] * 0.8

fig.add_annotation(x=improving_x, y=improving_y, text="Improving<br>(Look to Buy)",

# showarrow=False, font=dict(size=14, color="blue"))

showarrow=False, font=dict(size=14))

return fig

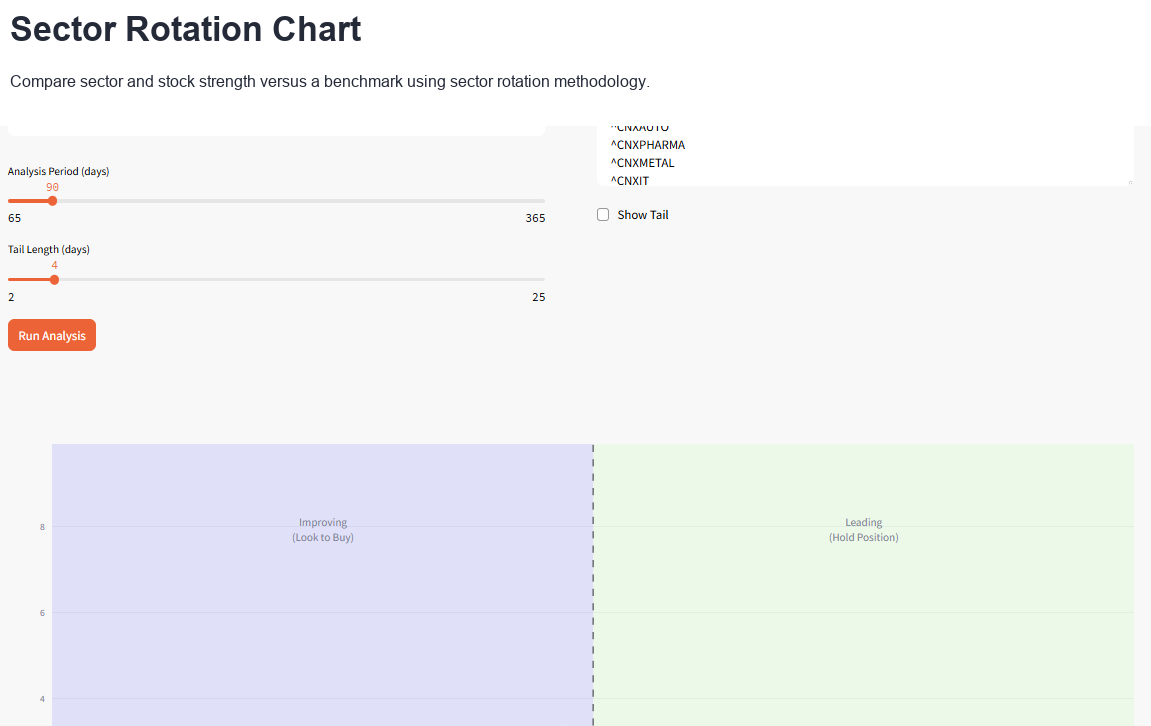

def main():

st.subheader("Sector Rotation Chart")

st.markdown(

"Analyze sector/stock performance relative to benchmark using sector rotation methodology. Input symbols as seen in Yahoo Finance")

col1, col2 = st.columns([1, 1], gap="large")

with col1:

# Benchmark input

benchmark = st.text_input("Benchmark Symbol", value="^NSEI",

help="Enter benchmark symbol (e.g., ^NSEI for Nifty 50)")

st.markdown("<style> .st-bu { background-color: rgba(0, 0, 0, 0); } </style>", unsafe_allow_html=True)

# Period slider

period = st.slider("Analysis Period (days)", min_value=65, max_value=365, value=90, step=5)

# Tail length slider

tail_length = st.slider("Tail Length (days)", min_value=2, max_value=25, value=4, step=1)

with col2:

# Sectors input

default_sectors = ["^CNXAUTO", "^CNXPHARMA", "^CNXMETAL", "^CNXIT", "^CNXENERGY", "^CNXREALTY", "^CNXPSUBANK",

"^CNXMEDIA", "^CNXINFRA", "^CNXPSE", "RELIANCE.NS", "INFY.NS"]

sectors_text = st.text_area(

"Enter Sector/Stock symbols (one per line)",

value="\n".join(default_sectors),

height=220,

help="Enter each sector/stock symbol on a new line"

)

sectors = [s.strip() for s in sectors_text.split('\n') if s.strip()]

show_tail = st.checkbox(label="Show Tail", value=False)

# Analysis button

if st.button("Run Analysis", type="primary"):

if not sectors:

st.error("Please enter at least one sector symbol")

return

with st.spinner("Fetching data and calculating metrics..."):

# Fetch benchmark data

benchmark_data, benchmark_failed = fetch_data([benchmark], period)

if benchmark not in benchmark_data:

st.error(f"Could not fetch data for benchmark: {benchmark}")

return

# Fetch sector data

sector_data, failed_sectors = fetch_data(sectors, period)

if not sector_data:

st.error("Could not fetch data for any sectors")

return

# Show warnings for failed symbols

if failed_sectors:

st.warning(f"Could not fetch data for: {', '.join(failed_sectors)}")

# Calculate relative rotation metrics

results = {}

benchmark_prices = benchmark_data[benchmark]

for symbol, prices in sector_data.items():

try:

# Calculate relative strength

rel_strength, rel_momentum = calculate_relative_strength(prices, benchmark_prices, 10)

if rel_strength is not None:

# Calculate JdK RS-Ratio and RS-Momentum

rs_ratio = calculate_jdk_rs_ratio(rel_strength)

rs_momentum = calculate_jdk_rs_momentum(rs_ratio)

results[symbol] = {

'rs_ratio': rs_ratio,

'rs_momentum': rs_momentum,

'relative_strength': rel_strength

}

except Exception as e:

st.warning(f"Error calculating metrics for {symbol}: {str(e)}")

continue

if not results:

st.error("Could not calculate metrics for any sectors")

return

# Create and display the plot

fig = create_sector_rotation_plot(results, tail_length, show_tail)

st.plotly_chart(fig, use_container_width=True)

# Summary table

st.subheader("Relative Positions of Sector/Stock")

summary_data = []

for symbol, data in results.items():

if data['rs_ratio'] is not None and data['rs_momentum'] is not None:

current_ratio = data['rs_ratio'].iloc[-1] if len(data['rs_ratio']) > 0 else 0

current_momentum = data['rs_momentum'].iloc[-1] if len(data['rs_momentum']) > 0 else 0

quadrant, color, icon = get_quadrant_info(current_ratio, current_momentum)

summary_data.append({

'Sector': symbol,

'RS-Ratio': f"{current_ratio:.2f}",

'RS-Momentum': f"{current_momentum:.2f}",

'Quadrant': f"{quadrant}"

})

if summary_data:

df_summary = pd.DataFrame(summary_data)

st.dataframe(df_summary, use_container_width=True, hide_index=True)

# Explanation

with st.expander("Understanding the Sector Rotation Chart"):

st.markdown("""

**Quadrants Explanation:**

**Leading (Top-Right)**: High relative strength, positive momentum

- Sectors out performing benchmark with increasing momentum

**Weakening (Bottom-Right)**: High relative strength, negative momentum

- Sectors still out performing but losing momentum

**Lagging (Bottom-Left)**: Low relative strength, negative momentum

- Sectors under performing benchmark with decreasing momentum

**Improving (Top-Left)**: Low relative strength, positive momentum

- Sectors under performing but gaining momentum

**How to Read:**

- **RS-Ratio > 100**: Sector out performing benchmark

- **RS-Ratio < 100**: Sector under performing benchmark

- **RS-Momentum > 0**: Relative strength is improving

- **RS-Momentum < 0**: Relative strength is declining

- **Tail**: Shows the trajectory of sector movement over time

""")

if __name__ == "__main__":

main()More from Python

Finding the Most Liquid Equity ETFs in each Category using Python

Not all ETFs are created equal — especially when it comes to liquidity. While NSE provides a full ETF list, identifying the...

The Market’s Coiled Spring — Building the Momentum Squeeze Indicator in Python

Volatility doesn’t expand randomly — it contracts first. The Momentum Squeeze Indicator, popularized by LazyBear, is built on this simple but powerful...

Price Consolidation Boxes: Ranges, Breakouts, and Retests Using Python

Markets don’t trend most of the time — they pause, compress, and consolidate. Before every meaningful move up or down, price typically...