Algo Trading

The Phoenix Bird - Swing Trading Strategy - Backtested!

FabTrader

Introduction

Stock markets often overreact, causing certain stocks to drop significantly in price. However, some of these stocks quickly recover, presenting a potential trading opportunity. The Phoenix Bird strategy is designed to identify such stocks that have hit bottom but show signs of resurgence. By applying a systematic approach to detect these stocks, we aim to capitalize on their potential rebound.

Strategy Overview

- The Phoenix Bird strategy is a long-only swing trading strategy.

- It uses daily candlestick data and is executed at the end of the trading day to find possible entries for the next day's open.

- The goal is to identify stocks that have recently dropped sharply but show recovery signs.

Entry Rules

A stock qualifies for entry if it meets the following conditions at the end of the trading day:

- Rate of Change (ROC): The percentage difference between today's closing price and the closing price 14 days ago must be less than -20% (indicating a sharp drop). ROC indicator is available on Trading View as well.

- Momentum Improvement: The ROC today must be more positive than the ROC yesterday.

- Recovery Confirmation: The ROC today must also be more positive than the ROC three days ago.

If these conditions are met, the trade is entered at the next day’s market open.

Exit Rules

The trade will be exited under the following conditions:

- Target Price Hit: The target is 1x the Average True Range (ATR) value calculated at the time of entry.

- Stop Loss Hit: The stop loss is set at 2.5x the ATR value calculated at the time of entry.

- Time-Based Exit: If neither the target nor stop loss is hit, the trade will be automatically closed after 10 days.

Python Script to Back Test this strategy

Following is the python code to back test this strategy. Only change you may want to do this script is replace your own respective historic data function with the one given here.

"""

Strategy : Phoenix

Psychology : Sometimes stocks go down in price due to market over-reaction and recovers fast.

This strategy identifies such stocks that hit bottom but is showing signs of recovery.

Rules of strategy:

- This uses daily candles and is run at the end of day to identify potential entries for next day open.

- This is a long-only strategy and hence no shorts

- Strategy will be run after the market is closed for the day and the entry into stock is done the next day open if its satisfies the following conditions.

1. The Rate of change (which is the percentage difference in prices between today's close and close 14 days earlier) is less than -20

2. The Rate of change today is more positive than the rate of change the previous day

3. The Rate of change today is more positive than the rate of change 3 days earlier

- The Target is 1 times ATR range value. The ATR value is to be calculated at the time of entry and maintained at that level till the end of trade

- Stop loss is 2.5 times ATR range value as calculated at the time of entry

- The trade automatically closes if the trade is open for more than 10 days and both target and stoploss are not hit

Custom Modifications:

- Timelimit exit reduced to 10 days (from 20 days)

- Too few trades for -20 ROC limit. Changed it to -15.

"""

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from datetime import date

import seaborn as sns

class PhoenixStrategy:

def __init__(self, tickers, start_date, end_date):

self.tickers = tickers

self.ticker = None

self.start_date = start_date

self.end_date = end_date

self.data = None

self.trades = []

self.trade_stats = {}

def fetch_data(self):

# Replace this function below with your own function that fetches historic data from your respective broker/resource

self.data = Instruments.get_historical_data(self.ticker, self.start_date, self.end_date)

# print(f"Downloaded {len(self.data)} rows of data for {self.ticker}")

return self.data

def prepare_data(self):

# Calculate Rate of Change (ROC) for 14 days

self.data['ROC_14'] = self.data['Close'].pct_change(14) * 100

# Calculate ROC from 1 day ago and 3 days ago

self.data['ROC_14_prev'] = self.data['ROC_14'].shift(1)

self.data['ROC_14_prev3'] = self.data['ROC_14'].shift(3)

# Calculate ATR (Average True Range) for setting targets and stop losses

self.data['TR'] = np.maximum(

self.data['High'] - self.data['Low'],

np.maximum(

abs(self.data['High'] - self.data['Close'].shift(1)),

abs(self.data['Low'] - self.data['Close'].shift(1))

)

)

self.data['ATR_14'] = self.data['TR'].rolling(window=14).mean()

# Drop NaN values

self.data = self.data.dropna()

return self.data

def backtest(self):

# Initialize variables

in_position = False

entry_price = 0

entry_date = None

entry_atr = 0

target = 0

stop_loss = 0

days_in_trade = 0

for ticker in self.tickers:

self.ticker = ticker

self.fetch_data()

self.prepare_data()

# Loop through each day

for i in range(1, len(self.data)):

if i == len(self.data)-1:

break # End of data. Avoid error while calculating next_date

current_date = self.data.index[i]

prev_date = self.data.index[i - 1]

next_date = self.data.index[i + 1]

# If we're in a position, check if any exit conditions are met

if in_position:

days_in_trade += 1

high_price = self.data.loc[current_date, 'High']

low_price = self.data.loc[current_date, 'Low']

close_price = self.data.loc[current_date, 'Close']

# Check if target hit during the day

if high_price >= target:

self.record_trade(entry_date, current_date, entry_price, target, 'target', days_in_trade, entry_atr)

print("Target Hit", current_date)

in_position = False

days_in_trade = 0

# Check if stop loss hit during the day

elif low_price <= stop_loss:

self.record_trade(entry_date, current_date, entry_price, stop_loss, 'stop_loss', days_in_trade,

entry_atr)

print("SL Hit", current_date)

in_position = False

days_in_trade = 0

# Check if 10-day limit reached

elif days_in_trade >= 10:

self.record_trade(entry_date, current_date, entry_price, close_price, 'time_limit', days_in_trade,

entry_atr)

print("Time Limit Hit", current_date)

in_position = False

days_in_trade = 0

# If not in position, check entry conditions for next day

else:

# Check entry conditions

roc_14 = self.data.loc[prev_date, 'ROC_14']

roc_14_prev = self.data.loc[prev_date, 'ROC_14_prev']

roc_14_prev3 = self.data.loc[prev_date, 'ROC_14_prev3']

entry_condition = (

# roc_14 < -20 and # ROC is less than -20%

roc_14_prev < -15 and # ROC is less than -15%

roc_14 > roc_14_prev # ROC today > ROC yesterday

and roc_14 > roc_14_prev3 # ROC today > ROC 3 days ago

)

if entry_condition:

# Enter position at next day's open

entry_price = self.data.loc[next_date, 'Open']

entry_date = next_date

entry_atr = self.data.loc[current_date, 'ATR_14'] # Use ATR from previous day (at time of decision)

# Set target and stop loss

target = entry_price + (entry_atr * 1.0)

stop_loss = entry_price - (entry_atr * 2.5)

print("Entry Triggered for ", self.ticker," Date ", entry_date, " Price ", entry_price, " Target ", target, " Stop Loss ", stop_loss)

in_position = True

days_in_trade = 1

return self.trades

def record_trade(self, entry_date, exit_date, entry_price, exit_price, exit_reason, days_held, atr):

pnl = ((exit_price / entry_price) - 1) * 100 # Percentage gain/loss

pnl_r = pnl / (atr / entry_price * 100) # R multiple (profit in terms of ATR)

trade = {

'entry_date': entry_date,

'exit_date': exit_date,

'entry_price': entry_price,

'exit_price': exit_price,

'exit_reason': exit_reason,

'days_held': days_held,

'pnl_percent': pnl,

'atr_at_entry': atr,

'pnl_r': pnl_r

}

self.trades.append(trade)

return trade

def analyze_performance(self):

if not self.trades:

print("No trades were executed in the backtest period.")

return {}

# Convert trades to DataFrame for analysis

trades_df = pd.DataFrame(self.trades)

# Overall statistics

total_trades = len(trades_df)

winning_trades = len(trades_df[trades_df['pnl_percent'] > 0])

losing_trades = len(trades_df[trades_df['pnl_percent'] <= 0])

win_rate = winning_trades / total_trades if total_trades > 0 else 0

avg_win = trades_df[trades_df['pnl_percent'] > 0]['pnl_percent'].mean() if winning_trades > 0 else 0

avg_loss = trades_df[trades_df['pnl_percent'] <= 0]['pnl_percent'].mean() if losing_trades > 0 else 0

profit_factor = abs(trades_df[trades_df['pnl_percent'] > 0]['pnl_percent'].sum() /

trades_df[trades_df['pnl_percent'] <= 0][

'pnl_percent'].sum()) if losing_trades > 0 else float('inf')

# Total return calculation

initial_capital = 100000 # Assuming $10,000 starting capital

capital = initial_capital

equity_curve = [initial_capital]

for _, trade in trades_df.iterrows():

trade_return = trade['pnl_percent'] / 100 # Convert percentage to decimal

capital = capital * (1 + trade_return)

equity_curve.append(capital)

total_return_pct = ((capital - initial_capital) / initial_capital) * 100

# Calculate drawdown

peaks = pd.Series(equity_curve).cummax()

drawdowns = (pd.Series(equity_curve) / peaks - 1) * 100

max_drawdown = drawdowns.min()

# Calculate Sharpe Ratio (assuming 252 trading days in a year)

trade_returns = trades_df['pnl_percent'] / 100

sharpe_ratio = np.sqrt(total_trades) * trade_returns.mean() / trade_returns.std() if len(

trade_returns) > 1 else 0

# Group trades by exit reason

exit_reasons = trades_df.groupby('exit_reason').agg({

'pnl_percent': ['count', 'mean', 'sum']

})

# Average trade duration

avg_days_held = trades_df['days_held'].mean()

# R-multiple statistics

avg_r = trades_df['pnl_r'].mean()

# Store all stats in a dictionary

self.trade_stats = {

'total_trades': total_trades,

'winning_trades': winning_trades,

'losing_trades': losing_trades,

'win_rate': win_rate,

'avg_win_pct': avg_win,

'avg_loss_pct': avg_loss,

'profit_factor': profit_factor,

'total_return_pct': total_return_pct,

'max_drawdown_pct': max_drawdown,

'sharpe_ratio': sharpe_ratio,

'avg_trade_duration': avg_days_held,

'avg_r_multiple': avg_r,

'exit_reasons': exit_reasons,

'equity_curve': equity_curve

}

return self.trade_stats

def display_results(self):

if not self.trade_stats:

print("No analysis available. Run analyze_performance() first.")

return

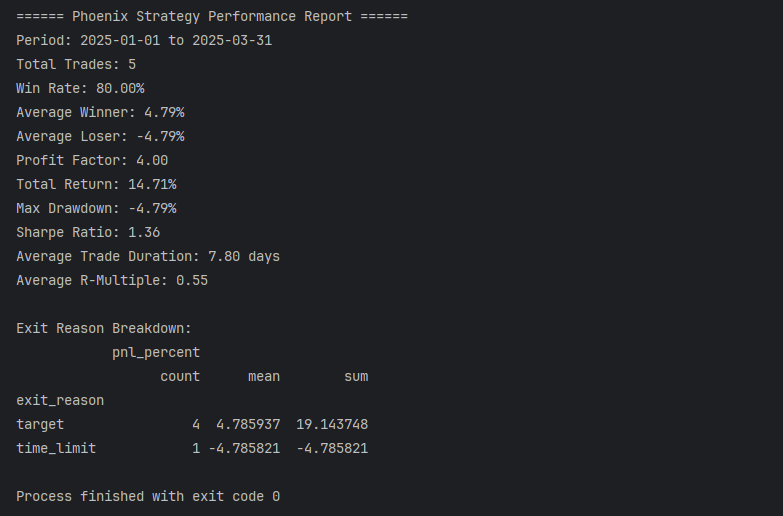

print("\n====== Phoenix Strategy Performance Report ======")

# print(f"Symbol: {self.ticker}")

print(f"Period: {self.start_date} to {self.end_date}")

print(f"Total Trades: {self.trade_stats['total_trades']}")

print(f"Win Rate: {self.trade_stats['win_rate']:.2%}")

print(f"Average Winner: {self.trade_stats['avg_win_pct']:.2f}%")

print(f"Average Loser: {self.trade_stats['avg_loss_pct']:.2f}%")

print(f"Profit Factor: {self.trade_stats['profit_factor']:.2f}")

print(f"Total Return: {self.trade_stats['total_return_pct']:.2f}%")

print(f"Max Drawdown: {self.trade_stats['max_drawdown_pct']:.2f}%")

print(f"Sharpe Ratio: {self.trade_stats['sharpe_ratio']:.2f}")

print(f"Average Trade Duration: {self.trade_stats['avg_trade_duration']:.2f} days")

print(f"Average R-Multiple: {self.trade_stats['avg_r_multiple']:.2f}")

# Display exit reason statistics

print("\nExit Reason Breakdown:")

print(self.trade_stats['exit_reasons'])

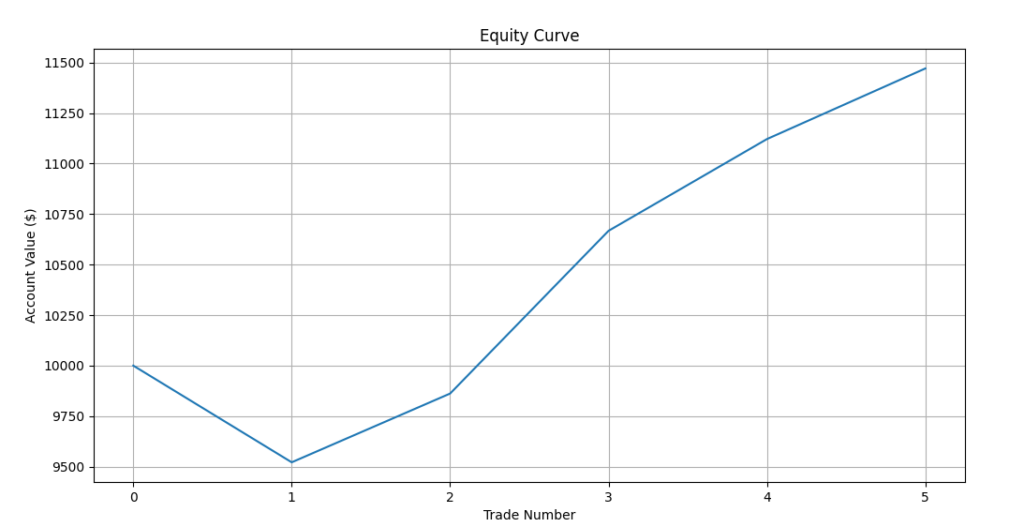

# Plot equity curve

plt.figure(figsize=(12, 6))

plt.plot(self.trade_stats['equity_curve'])

plt.title('Equity Curve')

plt.xlabel('Trade Number')

plt.ylabel('Account Value ($)')

plt.grid(True)

plt.show()

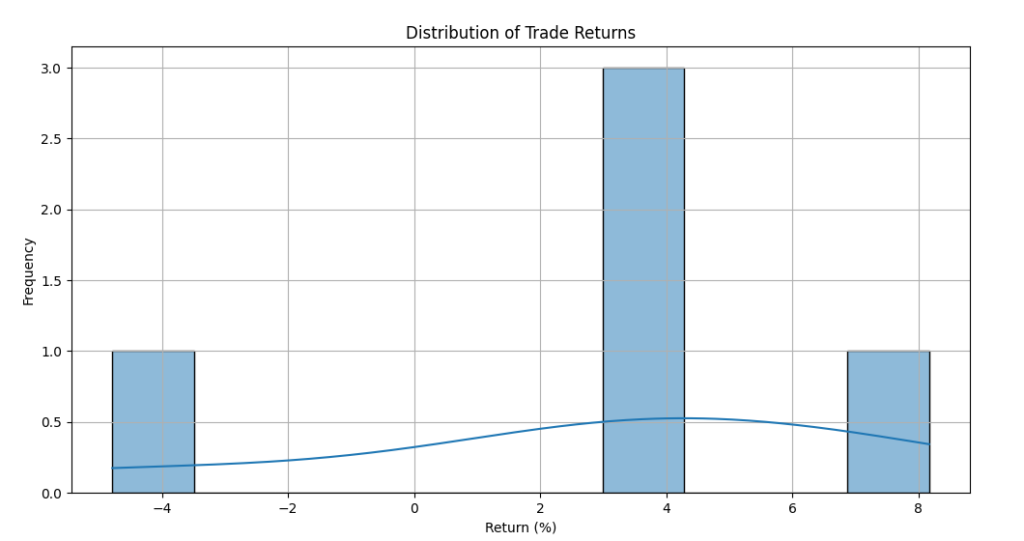

# Plot distribution of returns

plt.figure(figsize=(12, 6))

trades_df = pd.DataFrame(self.trades)

sns.histplot(trades_df['pnl_percent'], kde=True)

plt.title('Distribution of Trade Returns')

plt.xlabel('Return (%)')

plt.ylabel('Frequency')

plt.grid(True)

plt.show()

# Plot monthly returns

trades_df['month'] = pd.to_datetime(trades_df['entry_date']).dt.to_period('M')

monthly_returns = trades_df.groupby('month')['pnl_percent'].sum()

plt.figure(figsize=(12, 6))

monthly_returns.plot(kind='bar')

plt.title('Monthly Returns')

plt.xlabel('Month')

plt.ylabel('Return (%)')

plt.grid(True)

plt.xticks(rotation=45)

plt.tight_layout()

plt.show()

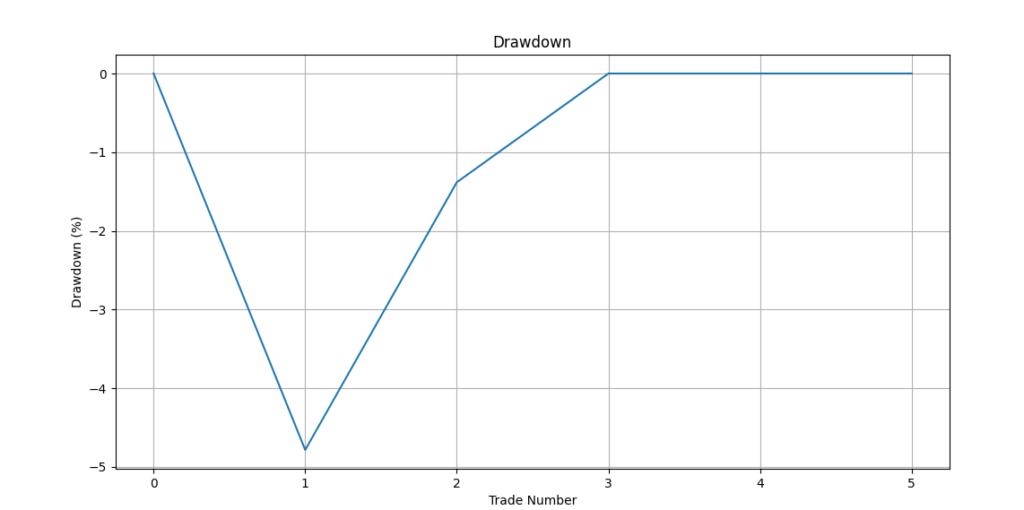

# Plot drawdown

equity_series = pd.Series(self.trade_stats['equity_curve'])

peaks = equity_series.cummax()

drawdowns = (equity_series / peaks - 1) * 100

plt.figure(figsize=(12, 6))

drawdowns.plot()

plt.title('Drawdown')

plt.xlabel('Trade Number')

plt.ylabel('Drawdown (%)')

plt.grid(True)

plt.show()

def run_full_backtest(self):

self.backtest()

self.analyze_performance()

self.display_results()

return self.trades, self.trade_stats

if __name__ == "__main__":

pd.set_option("display.max_rows", None, "display.max_columns", None)

tickers = [

"INFY", "ITC", "ASIANPAINT", "BRITANNIA", "ICICIBANK", "HCLTECH", "TCS", "LTIM", "TITAN",

"DRREDDY", "HINDUNILVR", "SBIN", "TATACONSUM", "HDFCBANK", "KOTAKBANK", "MARUTI", "BAJAJFINSV",

"SBILIFE", "LT", "NESTLEIND","AXISBANK", "CIPLA", "BHARTIARTL", "HEROMOTOCO", "GRASIM", "DIVISLAB",

"ADANIPORTS","TECHM","SUNPHARMA","EICHERMOT","INDUSINDBK","RELIANCE", "HDFCLIFE", "APOLLOHOSP",

"M&M","SHRIRAMFIN", "BAJFINANCE","POWERGRID", "ADANIENT", "BAJAJ-AUTO","WIPRO","ULTRACEMCO", "TATAMOTORS",

"NTPC", "COALINDIA", "ONGC", "HINDALCO", "BPCL", "JSWSTEEL", "TATASTEEL"

]

# Back Test period

start_date = date(2025, 1, 1) # Modify as needed

end_date = date(2025, 3, 31) # Modify as needed

strategy = PhoenixStrategy(tickers, start_date, end_date)

trades, stats = strategy.run_full_backtest()Back Test Results

With limited tests done, the strategy seems to be performing well. However, the number of trading opportunities seems low given that there would be very minimal occurrences of these scenario in market. With this free python back test code, you can run your own tests!

This is not a recommendation and use extreme caution and we advise you do your own research and back testing before using this strategy. This article is for educational purpose only and should not be construed as investment advice.

Key Takeaways

- The Phoenix Bird strategy focuses on mean reversion, capitalizing on market overreactions.

- By incorporating ATR-based targets and stop losses, risk is effectively managed.

- The time-based exit ensures that trades don’t remain open indefinitely.

- Backtest results suggest that this strategy has the potential to generate consistent swing trading opportunities.

How I Backtested This

I have a full-fledged backtesting framework in Python, built to test trading strategies with precision.

This is the same framework I teach in my course: Backtesting Trading Strategies using AI and Python. If you want to learn how to build such backtesters, test strategies like this one, and validate them with real numbers, you can check out the course here: [Link to Course].

And if you’re someone who wants to go one step further – not just test strategies but actually deploy them in real markets in full auto mode – I also run a course on Building a Complete Algo Trading System in Python.

In that program, I cover how to:

- Automate your strategies from end to end.

- Run them on an AWS server 24/7.

- Implement risk and money management.

- Build a real-time monitoring dashboard.

- Even manage trades from a Telegram bot.

Basically, it’s everything you need to go from a backtested strategy to a production-grade automated system. You can learn more about that here: [Link to Course].

Conclusion

The Phoenix Bird strategy is an effective way to identify stocks that have bottomed out and are poised for a rebound. By following a strict set of entry and exit rules, traders can systematically take advantage of these opportunities while maintaining proper risk management.

Would you like to explore this strategy further? Let’s discuss its real-world application and optimization in the comments!

More from Algo Trading

Algo Trading Cost in India: How I Built a Reliable Setup for ₹150/Month

Wondering how much algo trading costs in India? In this article, I break down the real expenses involved in running an algorithmic...

When Your Job Feels Shaky: Can Trading Become an Alternate Income Stream?

Can trading become a stable source of income in India? While many consider it during times of job uncertainty, the reality is...

How Much Capital Do You Really Need for Sustainable Trading Income in India?

How much capital is needed for sustainable trading income in India? This in-depth guide explores the realistic returns traders can expect, the...